Random thoughts

[Archive Post] Originally posted the July, 8 2019.

Post about the randomness factor of the Financial Markets.

Disclaimer : This is an old article, posted the January, 9 2017. Some information can be outdated.

Trying to become a true profitable trader and building your own trading system is a long and tedious journey. You will have tough periods climbing sloping mountains of doubts and fighting the wild psychological bias hidden in the bushes all along your travel. The obstacles on the path to victory are diversified and one of them can be very odorous : the scam. You will have to avoid to walk on it like dog poops.

Here’s a little article to help the investor and the rookie trader to detect and avoid them. You can use it on the track records you can see on every trading websites. This is a very simple scoring system where the 0 lets assume that the system is reliable and the 10 tells you to run away from the trading system.

Later, I’ll do an article to use efficiently the scamometer on trading websites.

We will start with a scamo-score of 0 and we will add points progressively trying to detect and dodge the best dog poops in the retail trading landscapes.

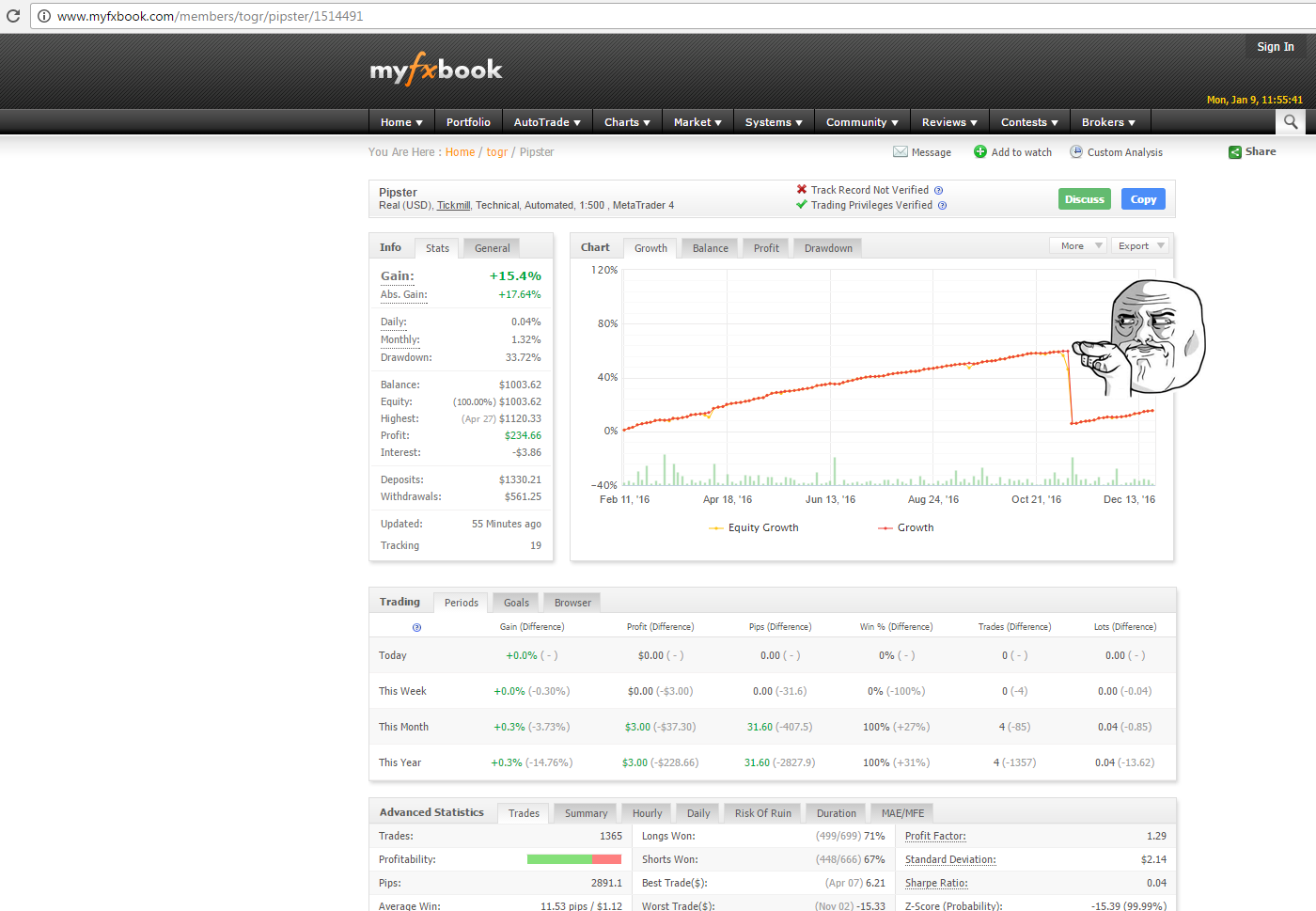

When you see a bleeding equity curve, you can ask yourself how the trader is managing the risk… Does he use stoplosses ? Does he hedges ? Does he keep positions opened during long time ? Does he accept the losses ? Does he like unicorns ?

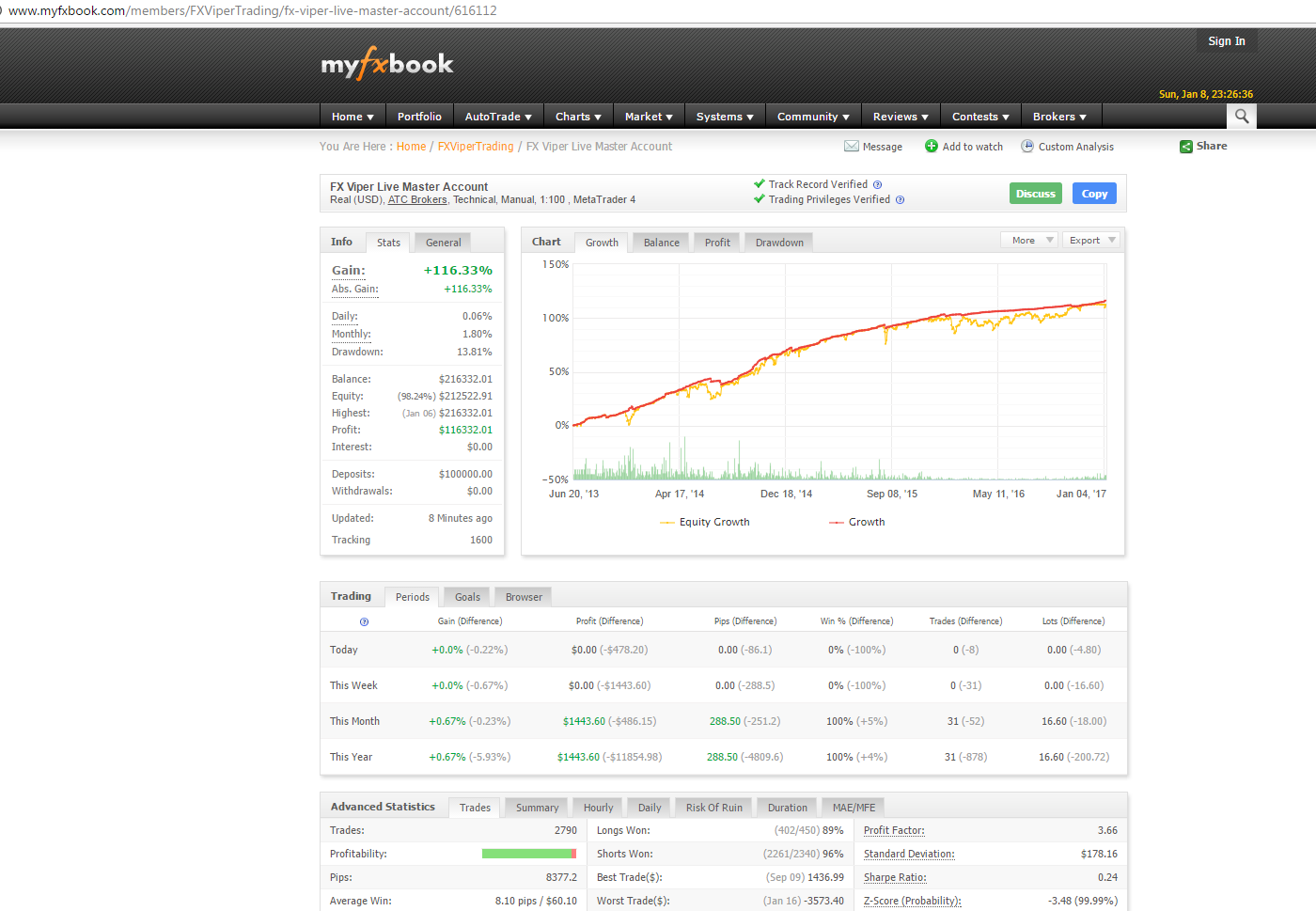

By seeing bleeding equity curve, you can add a +4 to the scamometer. I chose arbitrarily the most popular system on the Myfxbook website. The equity bleeds like an investor cutting his wrists:

When the growth curve is very sexy, appealing and hot, just like a linear curve, you can worry. Indeed, the track record shows in this case that the pseudo “trader” doesn’t accept the losses and is very likely not using stoplosses. This is very typical of the Martingale/Grids systems.

Give yourself a favor and add a nice 6 points to your scamometer when you see this :

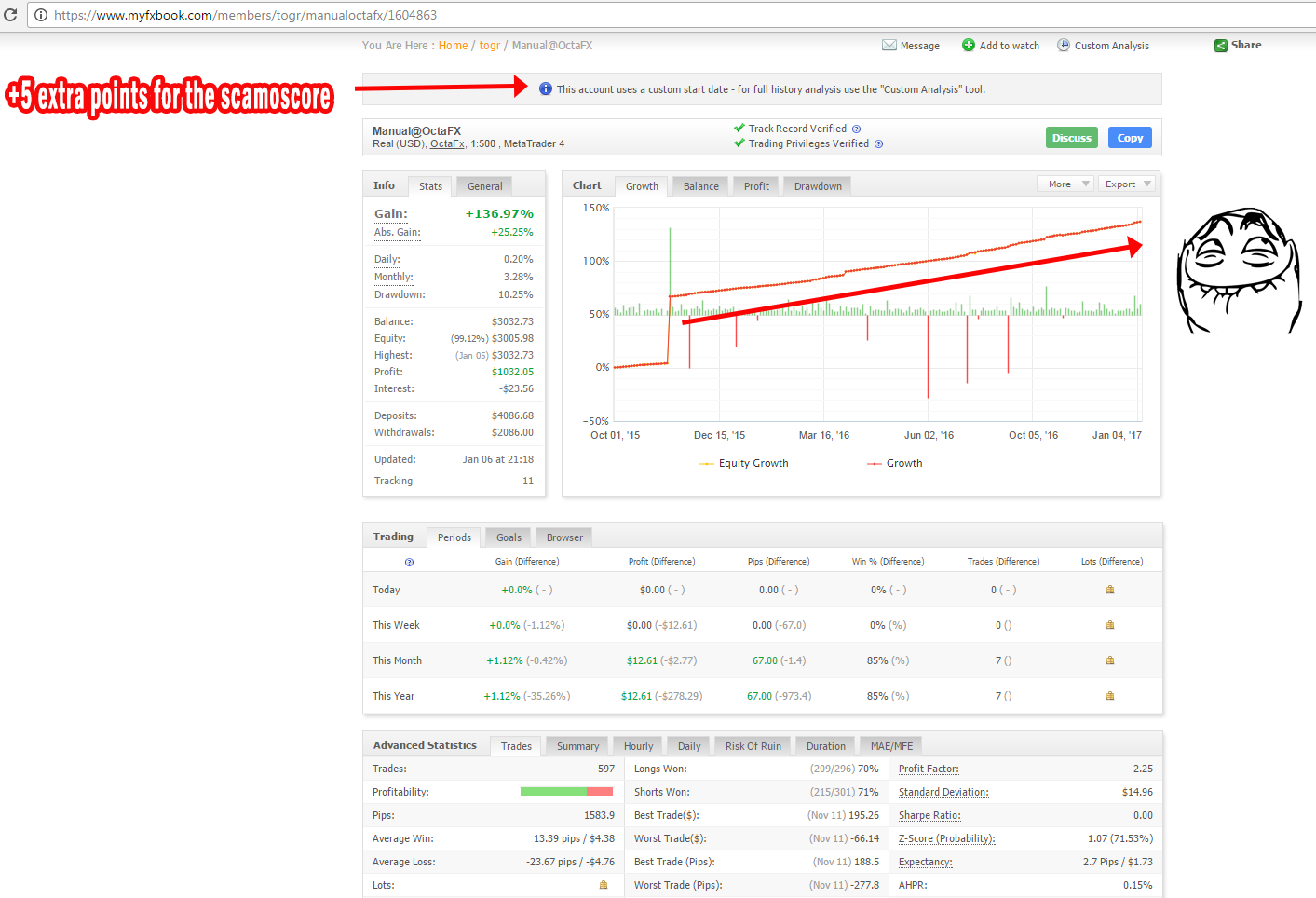

Sorry guys, the progression of a profitable system equity curve is never linear. Over the time, you’ll see this kind of thing (this other system is from the same scam-author than the previous one) :

The CRR (Chance/Risk Ratio) is a simple but efficient ratio calculated by dividing the percentage growth by the drawdowns. Thus, you have a quick estimate of risk and potential of the trading system. You can calculate it on a montly, yearly or historic basis to notice the evolution and the risk mitigation of the trader.

If the CRR is lesser than 1, you have a failing trading system in progress. This is cute to see. You can easily add a +2 to your scamo-score.

If the CRR is above 1, you have some kind of flat expectancy system but you have to confirm it with other metrics. This is quite neutral.

If the CRR is above 2-3, you start to see a decent trading system making money in theory. Again, you have to confirm this with other metrics.

When you assess a trading system, you have to read a short description to sum up the trading style of the trader (swing/scalper, fundamental/technical, …). The scamometer can detect some keywords in order to warn the investor against the shittiest systems. Here a sample of the interesting keywords :

Using the prefix “pseudo” before the 2 first keywords doesn’t change the score calculation.

But sometimes, the lack of certain keywords can increase drastically the scamoscore. For example, if you don’t find any information about stoplosses and you know that it’s some kind of UFO concept for the trader, you can add a nice +9 to the overall score. This remark can be moderated by the fact that instead of using stoplosses, true profitable traders can use hedging. However this is very specific, hard, and complex skills to master. The number of true profitable traders using successfully the hedging instead of the stoploss is equal to the number of finger on a hand of an armless person.

This is very important to identify how the trader sees the Markets and the risks associated. Its behavior and words are important too. You’ll find some “traders” being arrogant, proud and pretentious. All the true profitable traders I know have a common quality : they are humble. And on the Forex you have to be humble. You have to respect the Markets. Once you ended your journey by trading a profitable system, you become necessarily humble because of all the dusts you bit before achieving your goal.

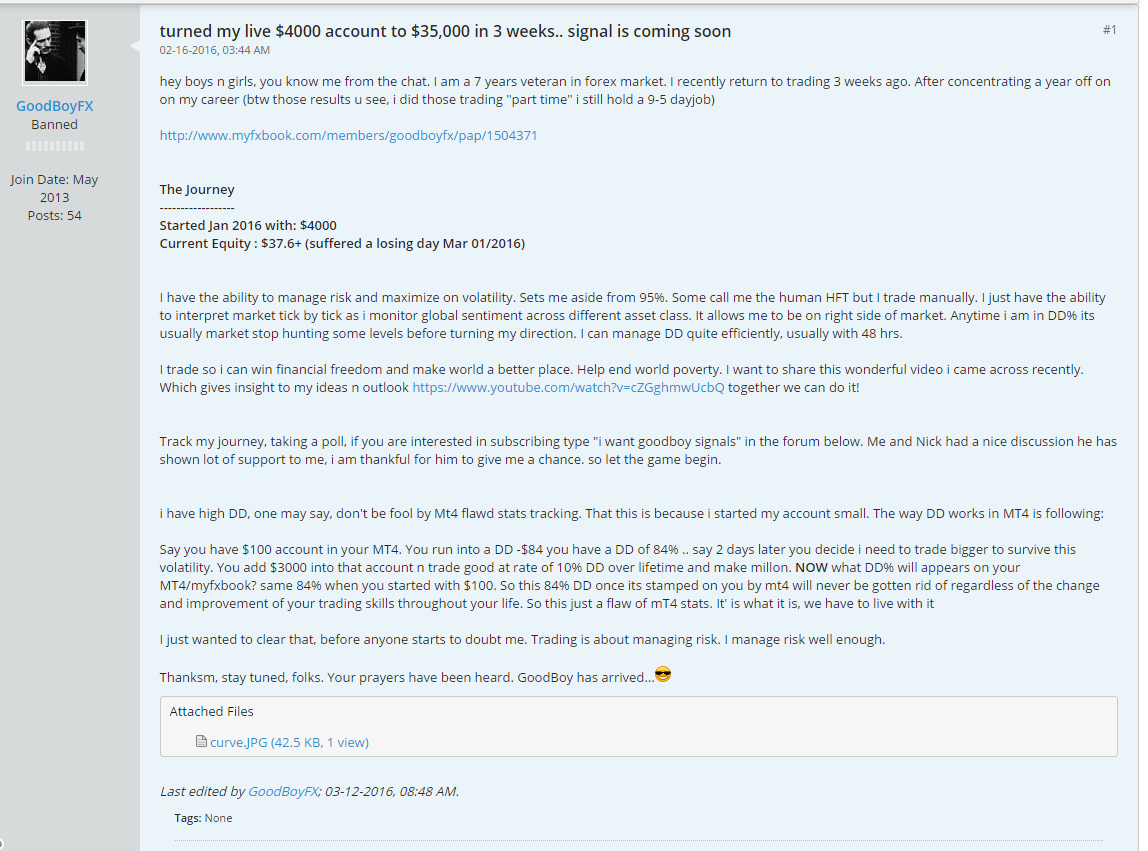

Here’s a funny story of a scam-trader offering its signal service on some signal forum community few months ago. You can see the bunch of common and basic psychological bias he had and its amateurism :

I don’t even talk about the huge and so risky performance he had. You can see the wizard explaining that he has a “gift” being able to know where the Markets will move :

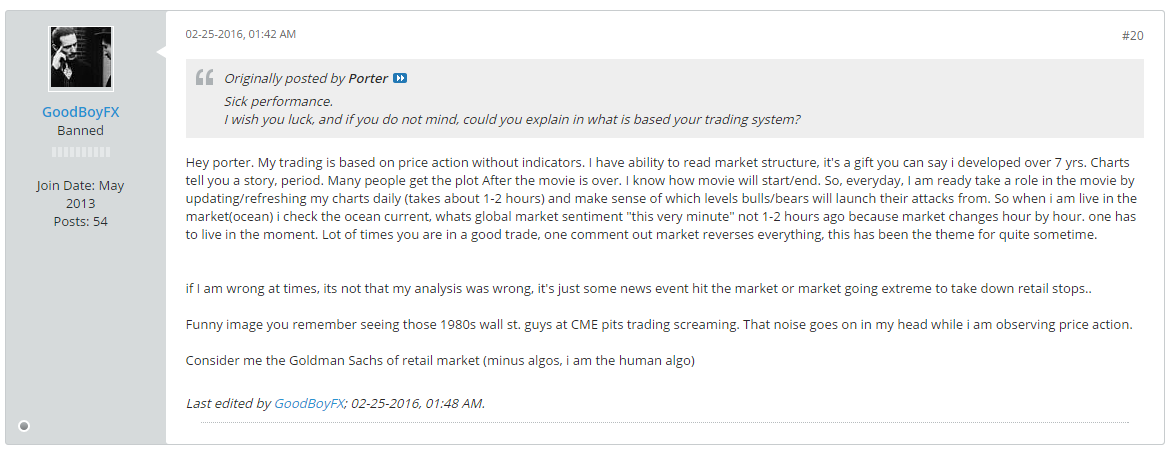

He self claimed being the “Goldman Sachs” of retail market. Such a gem. This one comes back regularly on the rookie traders forums. A lot of people want to trade for JPMorgan or Goldman Sachs banks. It looks like this is the edge of the trader carreer. But you can trust me, when you are a successful profitable and independant trader, you certainly don’t want to trade for these intitutions.

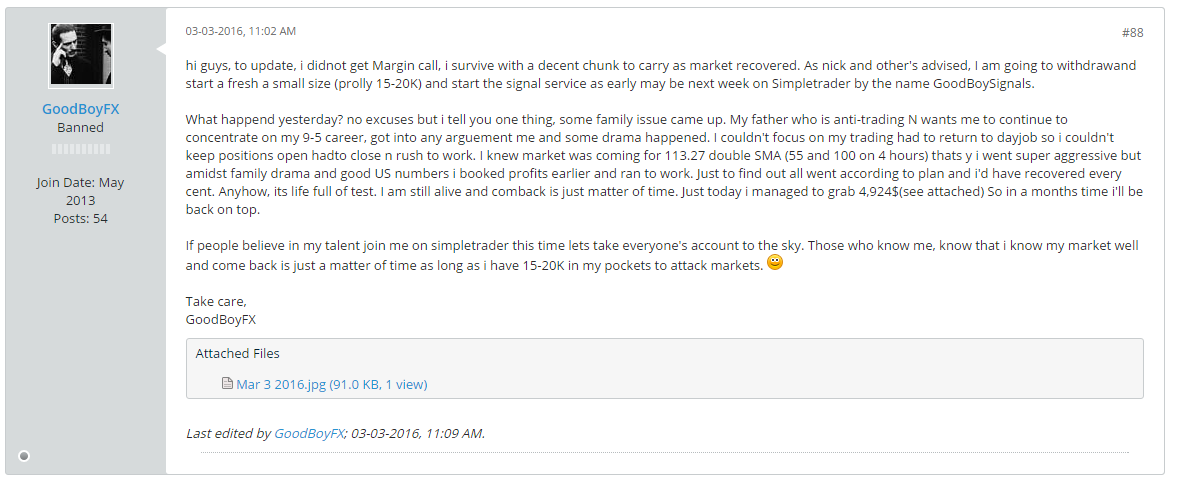

When some non expecting events occured, the “trader” finds excuses (very common psychological bias when you start trading is to not undertake your own responsabilities) :

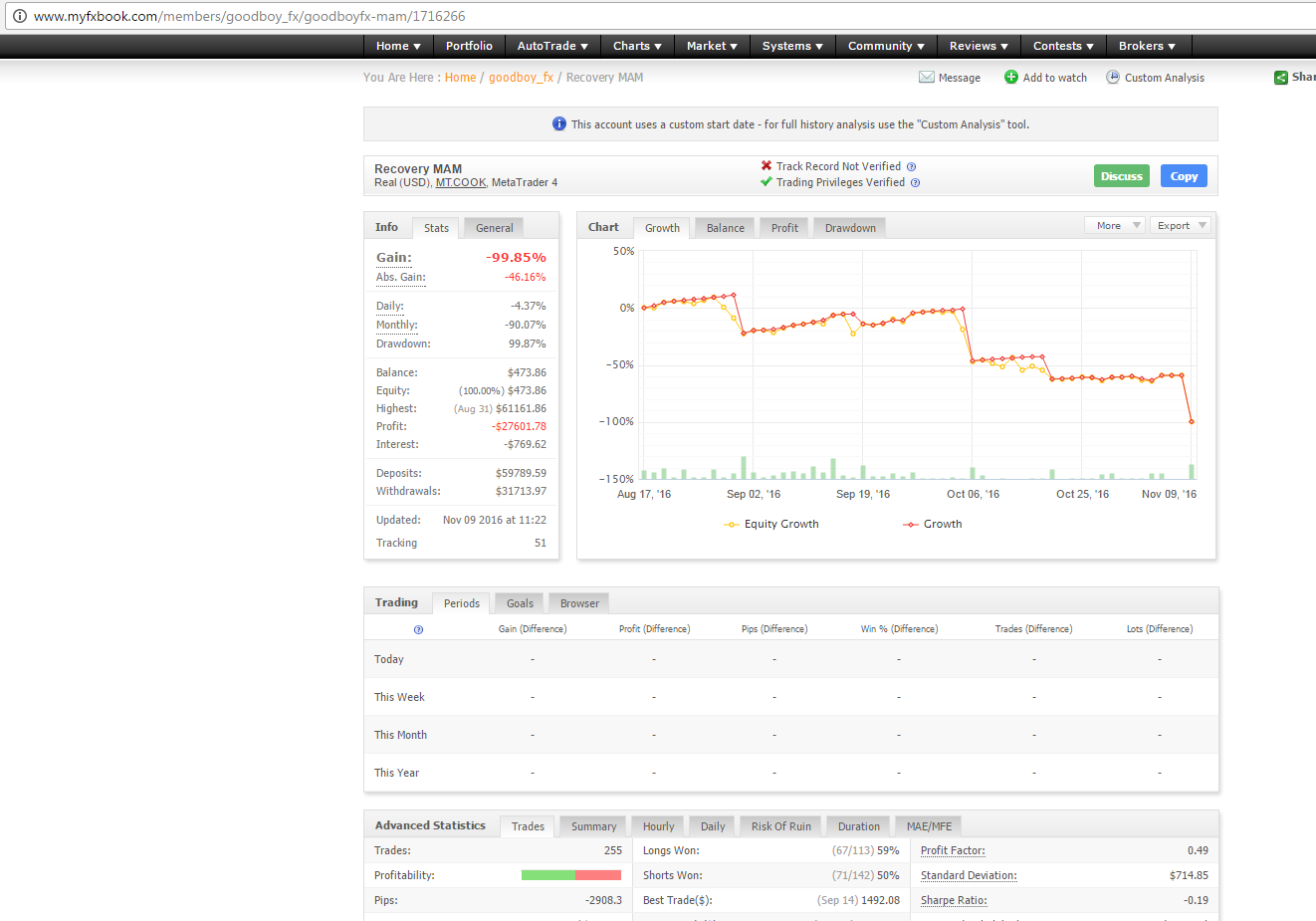

How this has ended ? With a lovely margin-call of course:

End of story. End of trader/investors money.

This rule is very easy to understand. If you find a system with a overall winratio higher than 90%, you can add +6 to your scamoscore.

Otherwise, it depends on the trading style of the system and especially the expectancy of the system. Considering a winratio without taking in account the R:R doesn’t make any sense.

Again, it’s a very simple and obvious rule to follow :

The backtest results are not considered by the scamometer. Backtest and demo trading are nothing compared to the real live trading.

By applying these weird and empirical calculation rules, you’ll have to say “Good bye” to your money in the future if the overall scamoscore is above 10.

Abracadabra… And it’s gone !

[Archive Post] Originally posted the July, 8 2019.

Post about the randomness factor of the Financial Markets.

[Archive Post] Originally posted the February, 12 2017.

Post about the interesting price structures which could lead to efficient trading setups.

[Archive Post] Originally posted the September, 7 2015.

Post about the importance of setting a stop loss to every Market orders in order to handle the risk.